What is a sole trader business? A great way to register as a sole trader in London

A sole trader is a self-employed person who runs and owns their own business by themselves. If you're a sole trader in London, you have no legal identity separated from your business. Due to this, many people describe sole traders as a business themselves.

In another article, we look in detail at sole trader advantages and disadvantages.

How does a sole trader differ to a limited company?

Overall, the main difference between a sole trader and a limited company is that a sole trader is owned and controlled by one individual. This means the person has unlimited liability for the business no matter the circumstance. On the other hand, a limited company has split ownership into equal shares between how many people are involved. This can help alleviate some strain and financial stress and leave you with less of a personal return at the end of each year.

Paying taxes as a sole trader

When it comes to tax and sole traders, things are done differently from a limited company.

As a sole trader you will need to make National Insurance Contributions (NICs). The amount you have to pay depends on the level of your earnings.Paying National Insurance contributions help you build up your state pension and benefits entitlement. If you’re a self-employed sole trader, your National Insurance costs are based around how much profit your business makes.

When it comes to tax, there are many rules and processes that go into being a self-employed, sole trader. A sole trader must pay tax on all their business profits. All taxable business profits are also subject to Class 2 and Class 4 National Insurance payments.

If you’re a sole trader in London, you can withdraw cash from your business without receiving any tax effect. Tax relief on interest and charges can be claimed if you’re a sole trader who has a separate personal banking account from their business account.

It’s worth noting that tax relief is given to sole traders on expenses exclusively for their business, meaning they won’t need to pay tax, or any tax they do pay will be reimbursed.

Another few points on tax as a sole trader are that when a sole trader sells their business or any assets, the monetary gain they receive will be taxed.

Read our sole trader vs limited company guide for more information.

Sole trader definition

A sole trader is a person who is self employed and runs the business alone needs to file self employed tax return.

Sole trader meaning

Sole trading refers to the legal structure of a business where an individual owns and runs a business alone. The person might employ other people.

Can sole traders employ staff?

The good news is that you can employ people and still trade as a sole trader. There isn’t a need to set up a limited company. As a sole trader you may operate your business on your own and make all the major decisions, but you don’t have to work alone. If you have or are planning to employ other people, they should be paid under Pay as You Earn payroll scheme for HMRC's income tax collection. Your accountant should be able to set this up for you and run your payroll for you.

The term 'sole trader' means that you are completing your business, trading as yourself under your own name.

How to come up with your sole trader business name

You should start thinking about your business name early on. Google company names, see what’s already out there, look at whether that company name website address (URL) is available, and it is worth looking at Companies House company name checker, just in case you do want to become a limited company in the future and see if the name is available.

Naming your sole trader business

When it comes to setting up your business name as a sole trader, there are a few rules you need to follow:

Sole trader names must not:

- Incorporate ‘limited’, ‘Ltd’, ‘limited liability partnership’, ‘LLP’, ‘public limited company’ or ‘plc’ within the company name.

- They must not be found offensive, such as using discriminating or offensive language.

- They must also not be the same as an existing trademark.

- The name that you choose for your business must also not contain any 'sensitive' word expressions.

They must also not suggest a connection with local authorities or the government unless you have received permission.

How do I register as a sole trader?

Ready to register as a sole trader with HMRC? If you want to register as a sole trader, you will need to complete a registration form via HMRC. This is so they are aware of your new business and expect a tax return from your earnings each year.

Sign up for self-assessment tax return

A self-assessment tax return is used to inform HMRC of an individuals or a sole trader's annual income regarding tax and national insurance liabilities. This sole trader registration form needs to be filled out and completed online, then submitted to HMRC before January 31st each year. To do this, you must fill out an SA100 form that considers other income such as from property, investments, as well as the money that has been earned through running a business.

Why do I need to fill in a self-assessment tax return?

The process of setting up and registering as a sole trader with HMRC is quite simple. Being a sole trader means that you are responsible for informing HMRC of your annual income every tax year. While standard employees get their national insurance and tax calculated for them, self-employed workers must complete a self-assessment every tax year so that HMRC can be informed and collect this owed money.

If you have earned less than £1,000, you may be exempt from this form, but it is worth checking out.

How to fill in your self-assessment

Here is a step-by-step guide in how to fill out your self-assessment tax return for and how to file it before the deadline of the tax year ends:

- Collect your information. Locate all the relevant information regarding your income. This includes any details of earnings and business expenditure.

- Fill in the form. When filling out the form, focus on the sections that are relevant to your own personal circumstance. If you're filling your form out online with your personal details, HMRC will remove any sections that are irrelevant to you.

- Report your earnings. Alongside all your collected information, you must submit your yearly earnings. If you have a separate job - income from employment must be given as well as capital gains, rent, pension income, investment income and any redundancies.

- Include tax-deductible expenses. Allowable expenses such as travelling, insurance, or marketing need to be added as these costs could be tax-deductible.

Do I need to register for VAT as a sole trader?

The answer to this question is in short, maybe. If you earn over £90,000 each year in annual turnover, you need to register for VAT.

If your business sells to other VAT-registered businesses, then you can register voluntarily. This can be a great way to reclaim any VAT that has been added within a sale. This is only if it suits your business and will not be suitable for everyone.

Do I need an accountant as a sole trader?

The answer depends on how much you know your money and tax issues. You are not required to have an accountant for your business accounts if you can do your own bookkeeping and tax return. But if you are unsure how much tax you need to pay or advice on all the expenses you can claim, then you’ll need someone hands on who knows accounting and tax to advise you. You can also forgo an accountant in your first year of business but to keep track of the annual accounts showing the flow of cash, expenses, and benefits after your business has grown you might need an accountant. The best way to keep track of the money flow is to have a separate bank account for your personal account and business transactions.

What are the main advantages of being a sole trader?

Apart from the total control and flexibility that comes with sole trading, there is a potential to earn more longer term, through running a business and the tax savings you can make. Keeping all your business's profits, setting up your own business is also relatively easy because you pay less to get things goings and you’re awarded with less administrative headaches.

Setting up as a sole trader is simple

If you’re branching out into sole trading, you won’t need to register with Companies House (as with a limited company) making the process quick and simple. However, you are required to inform HMRC of your self-employment status and that you are operating a business as a sole trader. You will not need to have a registered office to get started.

You are not required to register your sole trading name and can choose to use your own name or choose other options though they are certain rules to keep in mind when choosing the name. You are not allowed to include words like plc, Ltd or limited or offensive words in your sole trader name nor can you use an existing trade mark or a name linking to local authority without getting permission. The chosen name will need to appear on all official paperwork for example professional invoices and letters.

Sole traders have less admin

Since you only have to submit a self-assessment to HMRC, compared to the admin of a limited company set up, sole trader admin is much simpler. You won’t use loads of time on paperwork for Companies House, but you must ensure you keep good records and bookkeeping of all your sales and expenses.

Sole traders have fewer costs

Since you don’t pay anything to the Companies House when starting off the cost of set up is less than if you were going to trade as a limited company. Depending on the type of business you are running you might not need a huge amount of capital to start and run the business in its early stage. There are also savings on accountancy fees as a sole trader as you won’t have to submit a corporation tax return at your year end.

Sole traders have more privacy

Your financial information remains private if you are a sole trader as your details don’t appear on Companies House and hence your personal information and financial records are kept away from public view. Your personal details and financialsare much safer from inspection as you are required to publish your accounts at Companies House if you run a limited company.

Sole traders have complete control

You become your own boss. As a sole trader you won’t have any shareholders,directors, or bosses on your back questioning your decisions or asking for results. You have the final say in how you want your business to run.

Disadvantages of being a sole trader

If you are thinking of becoming a sole trader there some disadvantages that you should bear in mind. These are listed below and it’s important that you weigh them up against the advantages that come with being self-employed and decide what is better.

Unlimited liability

A business being run by a sole trader is not recognised as a separate legal entity, so the sole trader is personally liable for the business's debts and liabilities incurred. If the business does not take off or fails with debts, you will lose your income and will have to pay for the debts using personal assets that are not connected to the business. With unlimited liability you can lose valuable personal assets like your home or declare bankruptcy.

Tax limitations

If you are self-employed, you could pay more tax from your profits than those in limited companies would. For example you’ll pay income tax on your earnings whereas alimited company director can pay themselves dividends, which are generally taxed at a lower rate.

Problems with securing funding

The sole trader structure is considered more risky for banks and other financial organisations that you might want to access funds from. If you want to borrow money to raise your capital, then the accounting transparency that is associated with a limited company. but not a sole trader, will affect the amount of cash you may be offered by banks or financial institutions. The terms offered for you to access the loan might also differ to those offered to limited companies.

Sole traders might be able to access fixed rate loans but may not be able to access long-term finance loans or government schemes that are available for others. Since you cannot secure investments with shares or other financial securities, it’s always hard to secure large amounts of funding with good terms that can help grow your business.

More responsibility

While you might employ people to help you run the business all the big responsibilities and decisions rest on your shoulders. With no one else to brainstorm or bounce ideas off, you can be lonely and in need of further support.

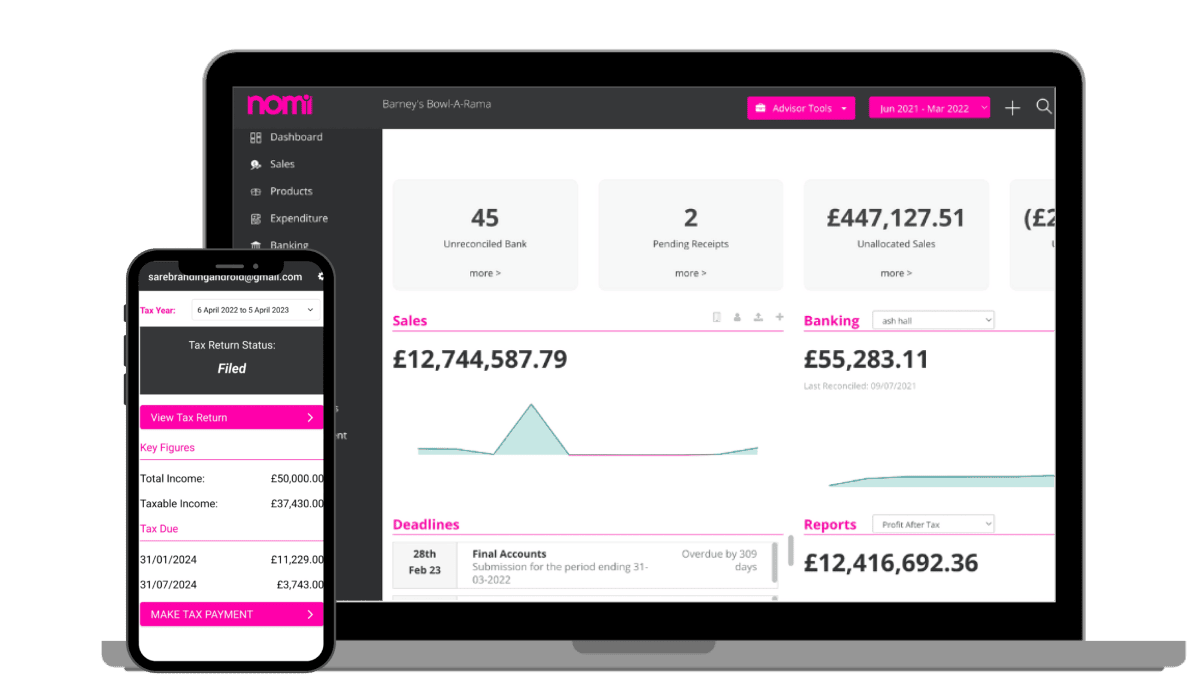

Free Business Software!

Say Goodbye to Bookkeeping Hassles: Nomi offers

accounting Free Receipt Processing and big savings!

Built in payment

solutions.

Hasslefree Bookkeeping

Snap pictures of

receipts using the

mobile app

Connect your bank

for easy reconciliation

Track your debtors

and creditors

Free Receipt Processing

Being a sole trader and being self-employed is similar but with some differences.

The words' sole trader' describes your business structure. Sole traders are self-employed people who are the sole owner of their business. Unlike limited companies, sole traders don't have to register with Companies House or have a director of the company.

A good example is if you're a freelance copywriter, you're self-employed but could describe your business structure as a 'sole trader'. It applies to many businesses, from running online shops, freelancing, or working as a self-employed electrician.

If you're self-employed, you're responsible for your success and failures, but you can operate under different business structures such as sole trader, partnership, or limited company. It can be regarding your business, the work style you do, when, and how you do it. You will not receive sick or holiday being self-employed, and you pay tax through self-assessment rather than using the PAYE system.

To summarise, the main difference between a sole trader and a self-employed is that 'sole trader' describes your business structure; 'self-employed' means that you are not employed by somebody else or pay tax through PAYE.

The kind of business sole traders are, means they are owned and managed by one individual. There is no legal distinction between the owner and the company, meaning that all debts and after-tax profits are personally yours. This style of outgoings and income is known as 'unlimited liability'.

Sole traders are responsible for nearly everything in their business. Your business's losses are entirely down to the owner, but this also means that any profit does not need to be shared with any other person.

Self-employment in this way also means you're responsible for any bills your company may concur with. Your annual profits, sales, and spending must be documented. If this isn't done correctly, you may find that your small business could be in trouble.

These forms must be completed annually to contribute and calculate your income tax, insurance, and other monies you may owe. You must also submit a self-assessment tax return to HMRC after registration, whether you're a sole trader or self-employed.

Since a sole trader business is not considered a separate legal entity to the owner, you become personally responsible for any business debts if you go bust. You will have to repay them from your personal account or risk bankruptcy. Hiring accountants in London can save you from these kinds of risks.

A limited company means it's a company with its own rights and is a legally distinct entity from the people who run it. If you run your business as a limited company, you can keep your company finances separate from yours and may also benefit from tax advantages.

Forming a limited company means you will have some benefits and drawbacks too.

These are the few advantages of becoming a limited company:

- Separate legal identity

- Limited owners liability

- Personal assets are protected

- Chances to raise new capital

These are the few disadvantages of becoming a limited company:

- More expensive

- More paperwork and financial document are involved

- Difficult to change the company structure

Sole traders pay tax on their profits which is tax-free below a certain amount for a year, and they also submit a self-assessment tax return to HMRC every year.

The process of switching from a sole proprietorship to a limited company in the UK is as follows:

Sole traders have to form a limited company and notify HMRC about this change. Apart from this, they need to be de-registered as self-employed.

No, there is no need for a separate business bank account. If sole traders have personal bank accounts, they can use those for business-related transactions. However, it is recommended to use business bank accounts to maintain the clarity of business transactions. Also, it is required to keep all receipts for the business expenses you claimed.

Still have questions?

See how dns can help

you today.

Do you need advice on being a sole trader. Our team at dns can give you all the help and advice you need. Give us a call today on 03300 886 686 to speak to our advisors, we'll find the right solution to all your sole trader needs.

Award-winning experts trusted by many

We're proud to be amongst the best accountants in the UK, demonstrated by the number of awards we've won over the years. We're also a top-100 accounting firm.

Here’s what our clients say

“I recently started my own company and in need of a good accountant. With my friends reference, I started dns accountancy services and I am a quite satisfied with their service. My account manager Sneha Gurudutta was always responsive and guided me a lot especially during my company early days. Keep u the good work.”

Here’s what our clients say

“I have been DNS for the last 3 months and I am very happy with the service. My account manager Sneha Gurudutta guided me and helped me with all the major/minor steps with the account setup. The weekend support they provide is really helpful. I would definitely recommend DNS to all my friends.”

Here’s what our clients say

“Unfortunately my son passed away without leaving any contact name of his accountant. I was able to make contact with the firm through HMRC. The staff were very prompt, caring and supportive in settling his income tax account. I was extremely impressed with the efficient caring and supportive service received from all of DNS staff.”

Here’s what our clients say

“Been with DNS Accountants for more than a year I would highly recommened their services. My account manager Sneha has been very helpful and helped with accounts and queries swiftly always! Having a good accountant means you can fully focus on your business, not worry about accounts and tax matters. Thank you DNS :-)”

Here’s what our clients say

“I have been extremely satisfied with the service I have been receiving close to past 1 year. Very professional, transparent and helpful. Special mention of my Account Manager Minakshi Arora who made my transition very smooth and always ready to go that extra mile to support and make customer happy. Definitely recommended.”

Here’s what our clients say

“I've recently set up a Ltd. Company and signed up with DNS for my accounting services. I've found it very good value for money and hugely helpful in terms of advice and guidance. I have a named Account Manager, Sneha Gurudutta, who keeps in contact with me and offers advice on line and on the phone... I'm really pleased with the service.”

Free Business Software!

Limited time only!

Free Business Software

Say Goodbye to Bookkeeping Hassles: Nomi offers Free Receipt Processing and big savings!

- Built in payment solutions.

- Track profitability, debtors and creditors

- Snap pics of receipts with the mobile app

- Free Receipt Processing

- Hasslefree Bookkeeping

- Cost Reduction

Close